The Hidden Opportunities in Bio-Based Ethylene That Most Investors Are Missing

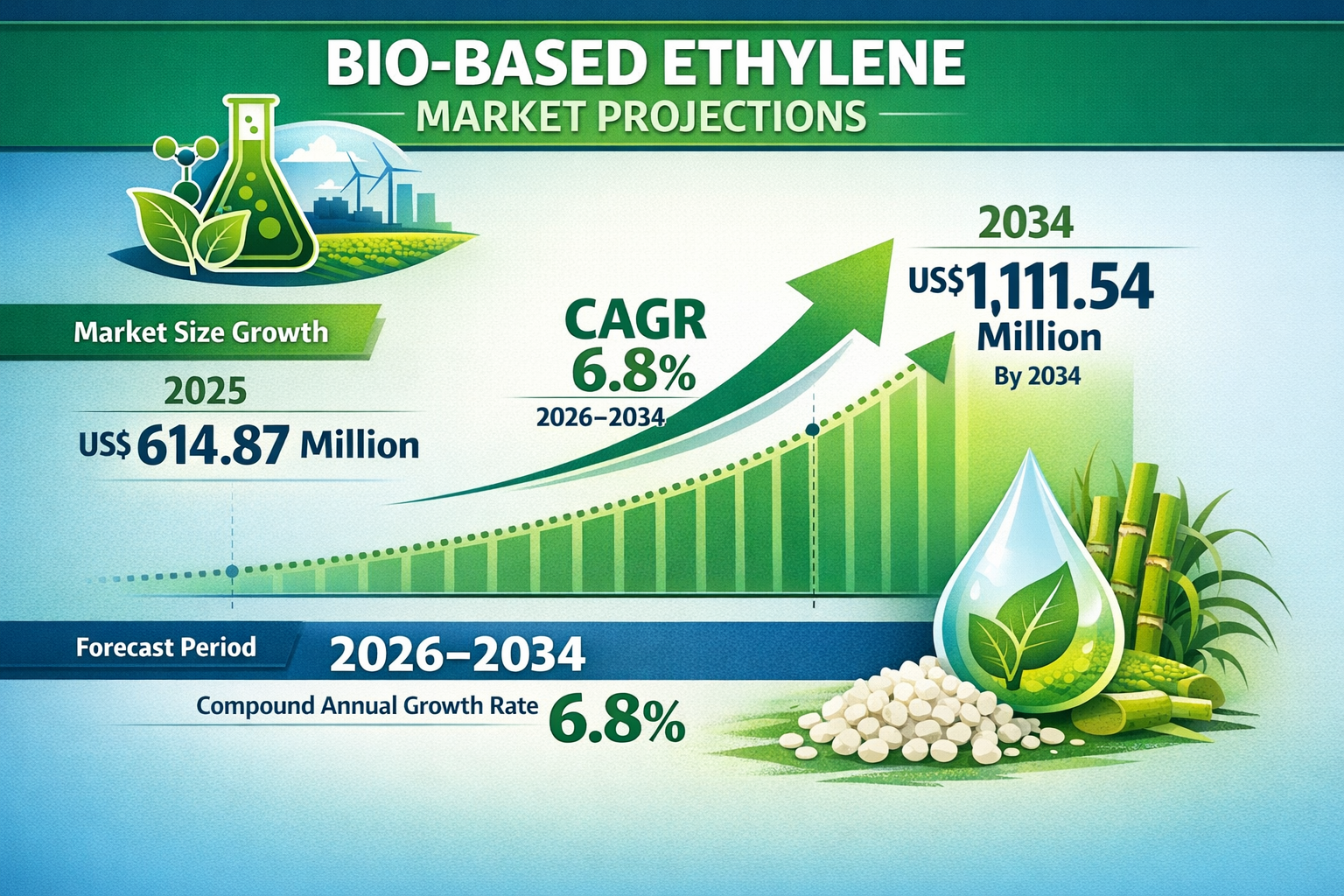

Growing from US$ 614.87 million in 2025 to US$ 1,111.54 million by 2034 at a CAGR of 6.8%, the bio-based ethylene market presents commercially significant opportunities in second-generation feedstock development, bio-based ethylene oxide and glycol derivatives, SAF byproduct integration, mass balance market entry, and ISCC PLUS certification-enabled premium positioning across sugars, starch, and lignocellulosic biomass raw materials and packaging, detergents, lubricant, and additives end-user industries. The Bio-Based Ethylene Market intelligence by The Insight Partners maps these opportunities through 2034.

The most commercially significant opportunities in bio-based ethylene are not in the segments where current market attention is concentrated. The packaging application and sugar feedstock pathway receive the majority of commercial and analytical attention, but the most differentiated and defensible opportunities for new market entrants and strategic investors lie in the underserved application categories and the emerging feedstock pathways where competitive intensity is lower and margin structure is more attractive.

Request Sample Pages of this Research Study @ https://www.theinsightpartners.com/sample/TIPRE00015881

Key Market Players

- Braskem S.A.

- The Dow Chemical Company

- LyondellBasell Industries Holdings B.V.

- SABIC

- Enerkem

- Linde

- Shell Global

- TotalEnergies

- Axens

Segments Covered

By Raw Material:

- Sugars

- Starch

- Lignocellulosic Biomass

By End-User Industry:

- Packaging

- Detergents

- Lubricant

- Additives

What makes the bio-based ethylene oxide and glycol derivative market an underexploited strategic opportunity?

While polyethylene is the primary outlet for bio-based ethylene and receives commensurate competitive attention, the bio-based ethylene oxide and glycol pathway serves the detergents and lubricants sector in ways that are significantly underserved by current market participants. Bio-based ethylene oxide serves as a precursor for renewable surfactants, allowing home care brands to claim fully bio-based formulations for their liquid soaps and laundry products. Bio-based glycols serve the textile and antifreeze sectors with renewable credentials that are growing in commercial value as scope three emissions reporting requirements expand. Companies that invest in the ethylene oxide and glycol derivative pathway now are building market positions in premium application categories before competitive intensity reaches the levels observed in commodity packaging.

The integration with SAF production creates a strategic opportunity that is available to petrochemical companies with existing steam cracker infrastructure but requires a commercial model that most have not yet developed. As aviation fuel producers scale SAF production and generate bio-naphtha byproduct, petrochemical companies that establish purchase agreements for this byproduct and develop the process integration to blend it into their steam cracker feedstocks are accessing bio-attributed ethylene at economics that may be more competitive than dedicated bio-ethanol routes in some markets. Developing this model requires cross-industry commercial relationship building that most chemical companies have not prioritised, creating a first-mover advantage opportunity for those who act early.

How does the Inflation Reduction Act create a specific investable opportunity in bio-based ethylene?

The production tax credit structure under the Inflation Reduction Act creates investment cases for bio-based ethylene production facilities in the United States that are genuinely attractive for projects that can qualify for the available incentive categories. Companies that develop project structures capable of capturing these incentives, combined with offtake agreements with US-based brand owner customers committed to renewable packaging targets, are building investment cases that may attract sustainable finance capital at terms unavailable to equivalent projects in jurisdictions without comparable policy support.

Also Available in: Korean | German | Japanese | French | Chinese | Italian | Spanish