Heat Transfer Fluids Market to Reach USD 12,400 Million by 2034 Amid Rising Demand for Advanced Thermal Management

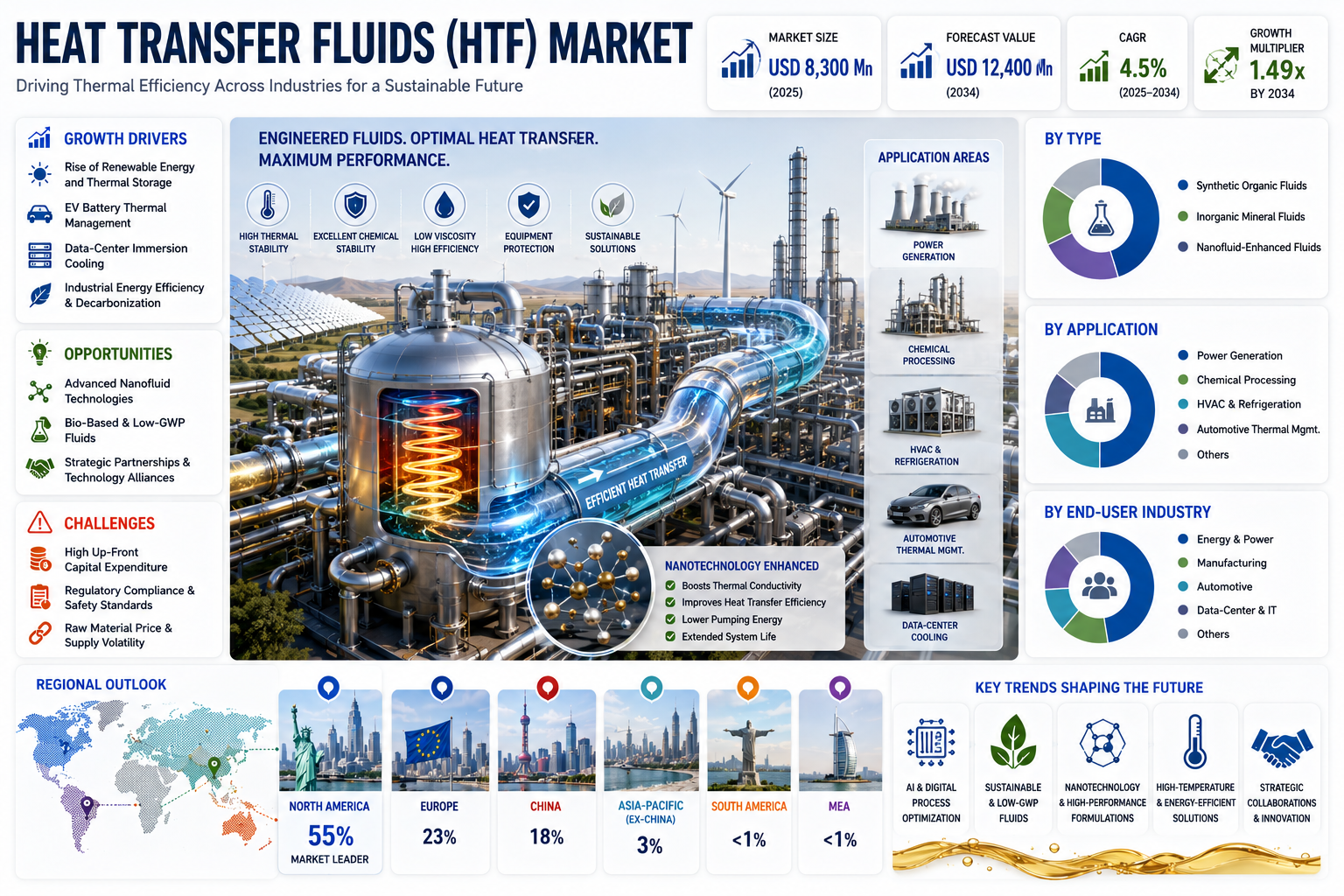

Global Heat Transfer Fluids (HTF) market was valued at USD 8,300 million in 2025 and is projected to reach USD 12,400 million by 2034, exhibiting a remarkable CAGR of 4.5 % during the forecast period.

Heat Transfer Fluids, a broad class of engineered liquids designed to transport thermal energy efficiently across a wide variety of industrial equipment, have moved from niche specialty chemicals to essential components in power generation, chemical processing, HVAC, automotive and emerging data‑center cooling applications. Their unique properties-including high thermal conductivity, chemical stability at elevated temperatures, low viscosity, and compatibility with a range of metals and seals-make them indispensable for maintaining precise temperature control, improving energy efficiency, and extending equipment life. Unlike traditional mineral oils, modern synthetic HTFs can operate at temperatures exceeding 400 °C while delivering superior heat‑transfer rates and reduced oxidative degradation.

Get Full Report Here: https://www.24chemicalresearch.com/reports/315725/heat-transfer-fluids-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Rise of Renewable Energy and Thermal Storage: Concentrated Solar Power (CSP) plants, geothermal installations, and emerging thermal‑energy‑storage systems depend on HTFs that can sustain high temperatures with minimal degradation. The global renewable‑energy capacity grew by over 10 % in 2023, and CSP projects in Spain, the United Arab Emirates and the United States are commissioning new HTF loops, driving demand for high‑temperature synthetic fluids that can operate safely above 350 °C.

- Electric Vehicle (EV) Battery Thermal Management: As EV sales surpassed 10 million units in 2023, manufacturers are integrating sophisticated cooling circuits that use low‑viscosity, non‑flammable HTFs to regulate battery pack temperatures. Efficient thermal management extends battery life, improves performance, and meets stringent safety standards, creating a rapidly expanding niche for specialized coolant formulations.

- Data‑Center Immersion Cooling: The explosive growth of cloud computing has pushed data‑center operators to adopt liquid‑immersion cooling, where servers are submerged in dielectric HTFs. This technique reduces energy consumption by up to 40 % compared with traditional air‑cooling, prompting major technology firms to invest in high‑performance, low‑global‑warming‑potential (GWP) fluids that meet strict electrical insulation requirements.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/315725/heat-transfer-fluids-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

- High Up‑Front Capital Expenditure: Deploying closed‑loop HTF systems-comprising storage tanks, heat exchangers, pumps, and real‑time monitoring infrastructure-requires substantial investment. For many mid‑size manufacturers, the payback period can extend beyond five years, causing hesitation to upgrade from legacy mineral‑oil‑based circuits.

- Regulatory Compliance & Safety Standards: Stringent regulations on volatile organic compounds (VOCs), flame‑retardancy, and low‑GWP emissions are reshaping formulation requirements. Achieving certification under REACH in Europe, EPA standards in the United States, and similar frameworks in Asia can lengthen product development cycles and increase compliance costs.

Critical Market Challenges Requiring Innovation

Scaling production of high‑purity synthetic HTFs while maintaining batch‑to‑batch consistency remains a technical challenge. Traditional manufacturing lines often yield 60‑70 % usable product, and impurities can compromise thermal stability. Moreover, integrating HTFs into existing equipment frequently demands retrofits-such as pump upgrades or seal replacements-to accommodate differing fluid viscosities, adding complexity for operators.

Supply‑chain volatility also plays a role. The availability of specialty raw materials, such as high‑purity silicone or perfluorinated compounds, can fluctuate due to geopolitical tensions or raw‑material price spikes. This uncertainty drives manufacturers to seek more resilient sourcing strategies and invest in regional production capacities.

Vast Market Opportunities on the Horizon

- Advanced Nanofluid Technologies: Incorporating metallic or ceramic nanoparticles into HTFs can boost thermal conductivity by up to 30 % without substantially increasing viscosity. Pilot projects in solar‑thermal power plants and high‑temperature metallurgy have demonstrated efficiency gains, positioning nanofluids as a high‑value niche for early adopters.

- Bio‑Based and Low‑GWP Fluids: Growing environmental scrutiny is accelerating the shift toward biodegradable, bio‑derived HTFs that exhibit low global warming potential. Companies are leveraging renewable feedstocks such as plant‑based esters and fatty‑acid derivatives to create fluids that meet both performance and sustainability criteria.

- Strategic Partnerships and Technology Alliances: Collaboration between fluid manufacturers, equipment OEMs, and end‑user industries is intensifying. Over the past three years, more than 40 joint ventures and licensing agreements have been announced, facilitating faster time‑to‑market for application‑specific HTF solutions and sharing R&D costs.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Synthetic organic fluids, Inorganic mineral fluids, and Nanofluid‑enhanced fluids. Synthetic organic fluids currently lead the market because of their broad temperature stability, compatibility with modern equipment, and proven reliability across demanding industrial processes. Inorganic mineral fluids retain a niche due to their inherent fire resistance and lower cost, making them attractive for legacy installations. Emerging Nanofluid‑enhanced fluids are gaining attention for their superior thermal conductivity, enabling more efficient heat exchange while maintaining low viscosity, which supports higher flow rates and reduces pumping energy.

By Application:

Application segments include Power generation, Chemical processing, HVAC and refrigeration, Automotive thermal management, and Others. Power generation drives the market owing to stringent reliability requirements and continuous operation cycles where HTFs must sustain high thermal loads over extended periods. Chemical processing thrives on fluids that resist degradation from aggressive solvents and catalysts, fostering long service life. In HVAC and refrigeration, low‑viscosity fluids enable compact system designs and rapid response times, while automotive and data‑center cooling represent fast‑growing sub‑segments that demand high‑performance synthetic formulations.

By End‑User Industry:

The end‑user landscape includes Energy & Power, Manufacturing, Automotive, Data‑Center & IT, and Others. Energy & Power accounts for the major share, leveraging HTFs for turbine cooling, steam‑generation cycles, and thermal‑energy‑storage loops. Automotive manufacturers focus on fluids that support both engine cooling and advanced battery‑thermal‑management systems, emphasizing low viscosity and rapid heat dissipation. Data‑center operators are increasingly adopting dielectric HTFs for immersion cooling, reflecting the sector’s rapid expansion and the need for efficient, space‑saving thermal solutions.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/315725/heat-transfer-fluids-market

Competitive Landscape:

The global Heat Transfer Fluids market is moderately consolidated and characterized by intense competition, rapid innovation, and strategic diversification. The top three companies-Dow Chemical (U.S.), BASF (Germany), and Eastman Chemical Company (U.S.)-collectively command approximately 55 % of the market share as of 2024. Their dominance is underpinned by extensive IP portfolios, deep vertical integration from raw‑material sourcing to custom‑formulation, and broad global distribution networks that enable reliable supply to power‑generation utilities, petrochemical complexes, and high‑tech manufacturers.

List of Key Heat Transfer Fluids Companies Profiled:

● Dow Chemical (United States)

● Eastman Chemical Company (United States)

● BASF (Germany)

● Solvay (Belgium)

● Clariant (Switzerland)

● ExxonMobil (United States)

● Sinopec (China)

● Arkema (France)

The competitive strategy across the sector is overwhelmingly focused on R&D to enhance fluid performance, reduce environmental impact, and lower total cost of ownership for end users. Companies are also forging strategic vertical partnerships with equipment manufacturers, renewable‑energy developers, and data‑center operators to co‑develop application‑specific HTF blends, thereby securing future demand and differentiating their product portfolios.

Regional Analysis: A Global Footprint with Distinct Leaders

● North America: Is the undisputed leader, holding a 55 % share of the global market. This dominance is fueled by massive R&D investments, a robust chemical‑manufacturing ecosystem, and strong demand from power‑generation, automotive, and data‑center sectors. The United States serves as the primary engine of growth, with ongoing projects in CSP, advanced nuclear reactors, and large‑scale data‑center cooling driving fluid innovation.

● Europe & China: Together, they form a powerful secondary bloc, accounting for 41 % of the market. Europe’s strength derives from flagship initiatives such as the EU Horizon‑Europe research programmes targeting low‑GWP HTFs and high‑temperature silicone blends. China, backed by substantial government subsidies for renewable‑energy infrastructure, is a dominant producer and rapidly growing consumer, especially in CSP, geothermal, and automotive thermal‑management applications.

● Asia‑Pacific (ex‑China), South America, and MEA: These regions represent the emerging frontier of the HTF market. While currently smaller in scale, they present significant long‑term growth opportunities driven by rapid industrialization, expanding petrochemical complexes, and increasing investments in renewable‑energy projects and data‑center capacity across India, Southeast‑Asia, Brazil, and the United Arab Emirates.

Get Full Report Here: https://www.24chemicalresearch.com/reports/315725/heat-transfer-fluids-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/315725/heat-transfer-fluids-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/